Loading market data...

ADVERTISEMENT

Latest Top News

India’s Monetary Evolution: How Repo Rate Shifts Since 2000 Shaped Growth And Inflation Control

India’s repo rate history reflects the Reserve Bank of India’s evolving monetary policy over the past 26 years. From double-digit highs in the early 2000s to record lows during the pandemic, the repo rate has been a critical lever to balance inflation, liquidity, and growth.

Stay Ahead – Explore Now! L&T Technology Services Partners With Databricks for Industrial AI

ADVERTISEMENT

Latest Updates

Sarpreet Singh Makes History For New Zealand At FI...

16 Jun 2026, 09:00 AM

Mini Diamonds India Bags ₹162.5 Million Natural Di...

16 Jun 2026, 09:12 AM

Affle MEA Enters Agreement to Acquire AdColony Ass...

16 Jun 2026, 09:08 AM

Stocks to Watch Today: Bharti Airtel, HCL Tech, Ad...

16 Jun 2026, 08:56 AM

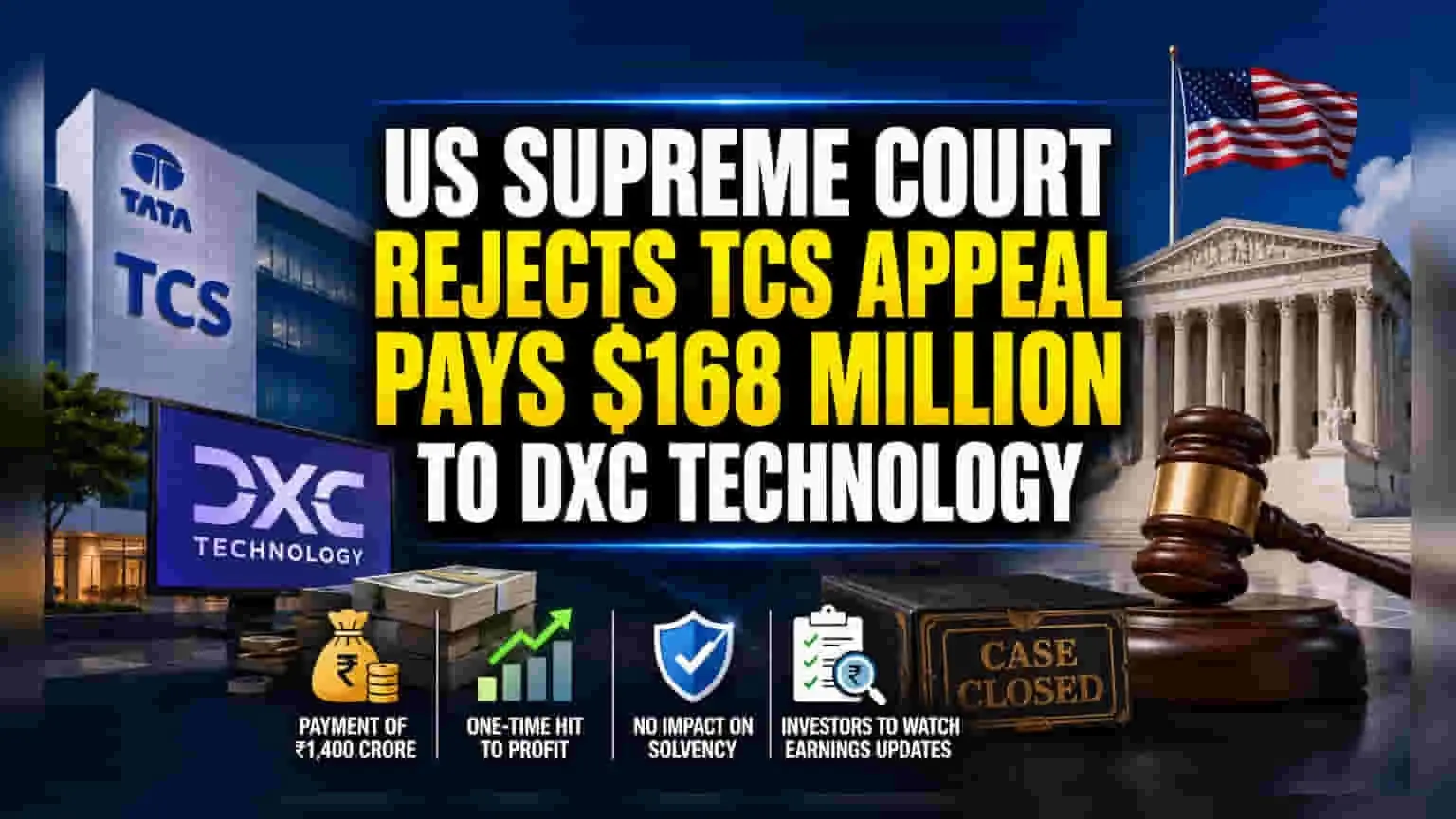

US Supreme Court Rejects TCS Appeal in DXC Trade S...

16 Jun 2026, 09:04 AMADVERTISEMENT

Top Stories

Sarpreet Singh Makes History For New Zealand At FI...

16 Jun 2026, 09:00 AM

Mini Diamonds India Bags ₹162.5 Million Natural Di...

16 Jun 2026, 09:12 AM

Affle MEA Enters Agreement to Acquire AdColony Ass...

16 Jun 2026, 09:08 AM