Loading market data...

ADVERTISEMENT

Latest Top News

State Borrowings Surge as SDL Yields Reflect Market Appetite and Tenor Dynamics

Key highlights from the latest Reserve Bank of India (RBI) auctions and yield movements paint a vivid picture of evolving risk perceptions and demand patterns in the state development loan (SDL) market.

Primary Market Yields Showcase State and Tenor Differentiation

- Tamil Nadu SDL 2...

Stay Ahead – Explore Now! Sycamore in Talks with Weston Family and Sigma Over £7.5B Boots Sale

ADVERTISEMENT

Latest Updates

Sarpreet Singh Makes History For New Zealand At FI...

16 Jun 2026, 09:00 AM

Mini Diamonds India Bags ₹162.5 Million Natural Di...

16 Jun 2026, 09:12 AM

Affle MEA Enters Agreement to Acquire AdColony Ass...

16 Jun 2026, 09:08 AM

Stocks to Watch Today: Bharti Airtel, HCL Tech, Ad...

16 Jun 2026, 08:56 AM

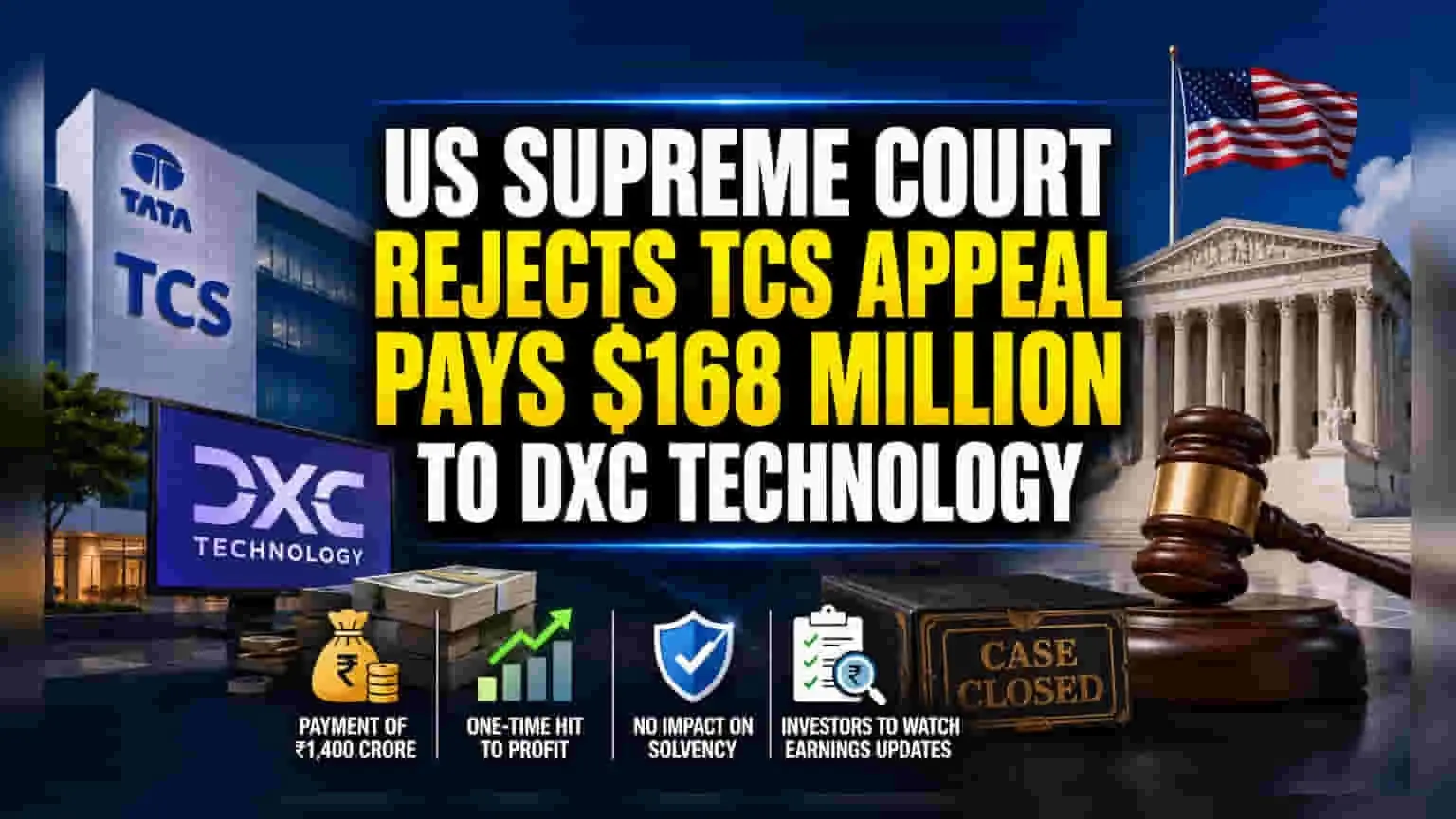

US Supreme Court Rejects TCS Appeal in DXC Trade S...

16 Jun 2026, 09:04 AMADVERTISEMENT

Top Stories

Sarpreet Singh Makes History For New Zealand At FI...

16 Jun 2026, 09:00 AM

Mini Diamonds India Bags ₹162.5 Million Natural Di...

16 Jun 2026, 09:12 AM

Affle MEA Enters Agreement to Acquire AdColony Ass...

16 Jun 2026, 09:08 AM