Loading market data...

ADVERTISEMENT

Latest Top News

The Big Retirement Question: Is Rs 20 Crore Enough To Live Comfortably In India?

A retirement corpus of Rs 20 crore may sound massive, but rising life expectancy, inflation, healthcare costs, and lifestyle expectations are reshaping financial planning in India. Experts warn that what once seemed sufficient may fall short, forcing individuals to rethink retirement strategies, savings goals, and long-term wealth planning.

Stay Ahead – Explore Now! Major Stocks Turn Ex-Dividend This Week: HDFC Bank, Tata Tech in Focus

ADVERTISEMENT

Latest Updates

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

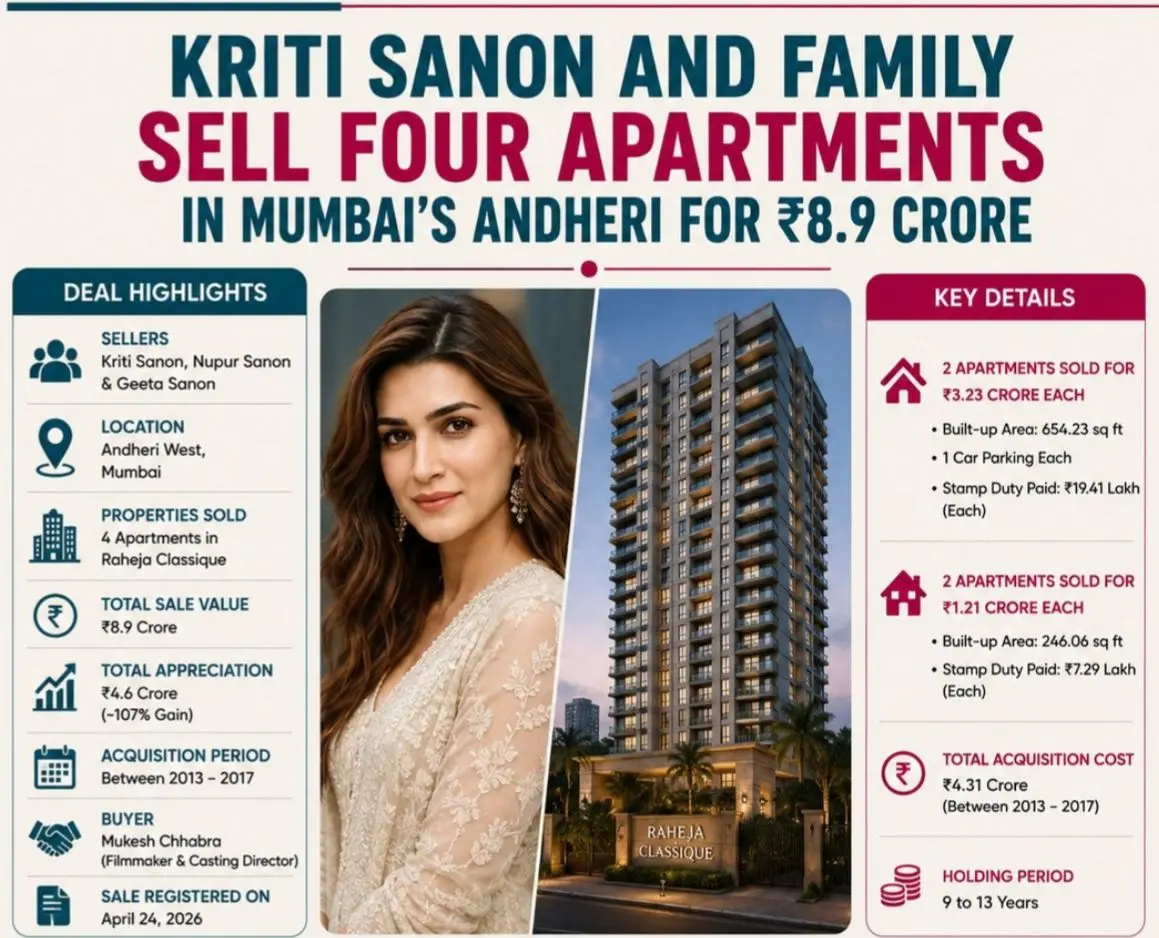

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PMADVERTISEMENT

Top Stories

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM