Loading market data...

ADVERTISEMENT

Latest Top News

Auto Pulse July 2025: Mixed Signals, Festive Hopes Drive Cautious Optimism in Indian Vehicle Market

India’s automobile industry posted a nuanced performance in July 2025, with growth in two- and three-wheeler segments offsetting a mild contraction in passenger vehicle sales. According to the Society of Indian Automobile Manufacturers (SIAM), the industry remains cautiously optimistic as t...

Stay Ahead – Explore Now! Zaggle Prepaid Ocean Services Seals 5-Year Deal with Crompton Greaves

ADVERTISEMENT

Latest Updates

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

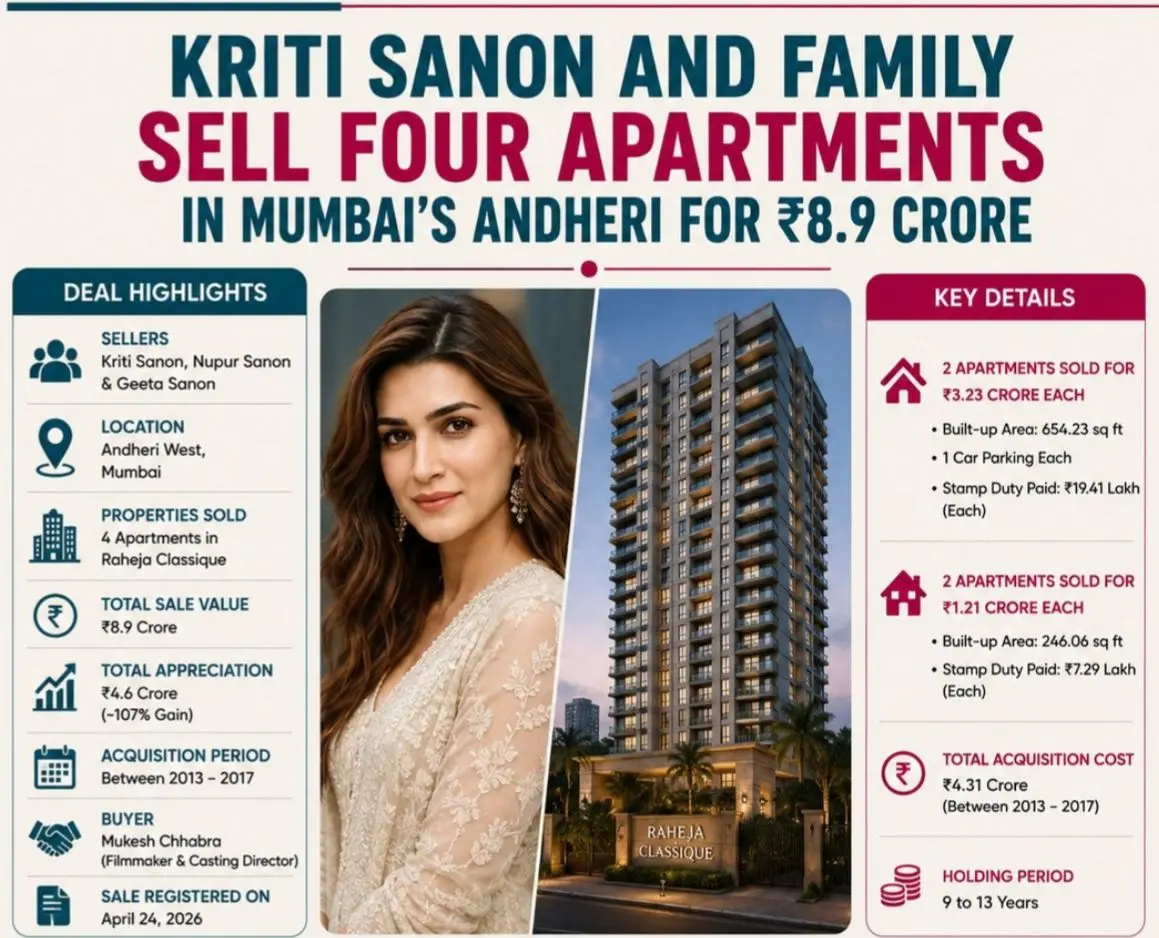

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PMADVERTISEMENT

Top Stories

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM