Loading market data...

ADVERTISEMENT

Latest Top News

IRCON International’s Q1 FY26 Results: Revenue Slump but Order Book Resilient

Marking an important quarter for India’s state-owned engineering and construction giant, IRCON International Limited Q1 FY26 financials highlighted a significant year-on-year contraction in operational performance. The company, renowned for its expertise in railways, highways, and turnkey i...

Stay Ahead – Explore Now! Monarch Surveyors Secures Maharashtra Green Roads Mandate

ADVERTISEMENT

Latest Updates

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

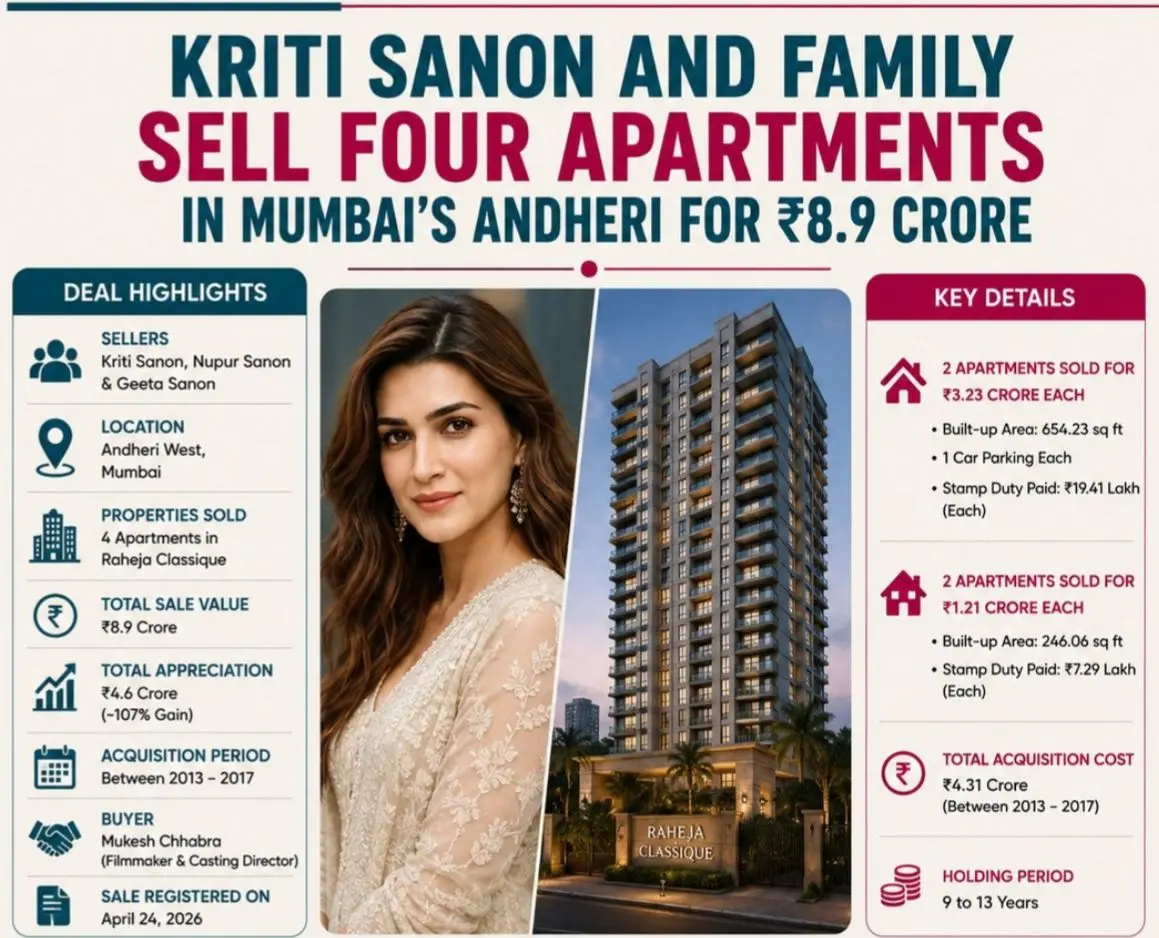

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PMADVERTISEMENT

Top Stories

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM