Loading market data...

ADVERTISEMENT

Latest Top News

Made in India, Made to Last: India’s Manufacturing Sets 17-Year Record with PMI at 59.1 in July

India’s manufacturing sector continued its robust expansion in July, with the final HSBC/S&P Global Manufacturing Purchasing Managers’ Index (PMI) settling at 59.1. Though slightly below the flash estimate of 59.2, the final reading still marks one of the strongest performances in...

Stay Ahead – Explore Now! Bombay High Court Upholds Arbitral Award for Siemens Energy

ADVERTISEMENT

Latest Updates

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

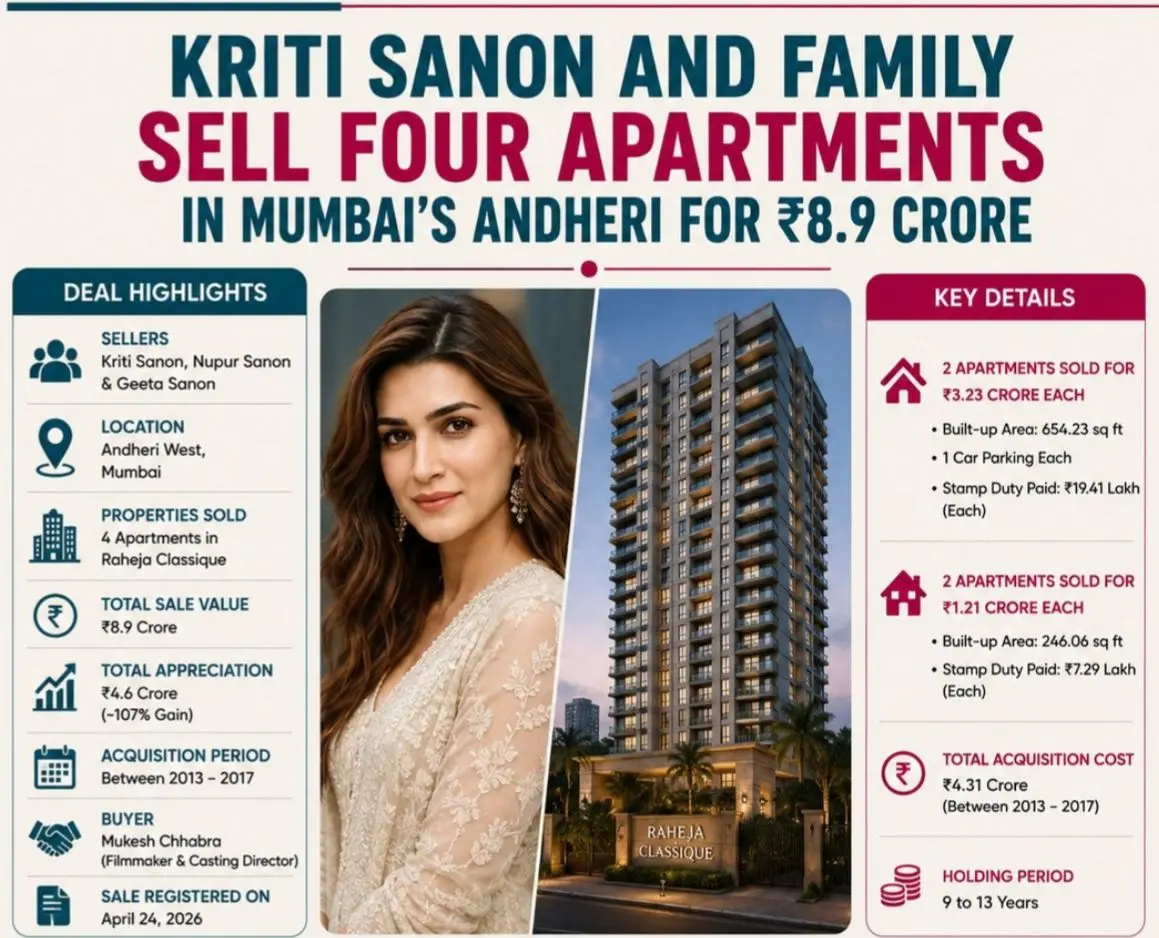

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PMADVERTISEMENT

Top Stories

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM