Loading market data...

ADVERTISEMENT

Latest Top News

Punjab & Sind Bank Total Business Reaches ₹2,66,574 Crore

Punjab & Sind Bank reported a 15.33% year-on-year increase in its provisional total business, reaching ₹2,66,574 crore for the quarter ended June 30, 2026. The growth was propelled by a 19.50% jump in gross advances, lifting the lender's credit-deposit ratio to 81.18%.

Stay Ahead – Explore Now! Nintec Systems Reappoints Niraj Gemawat as Managing Director

ADVERTISEMENT

Latest Updates

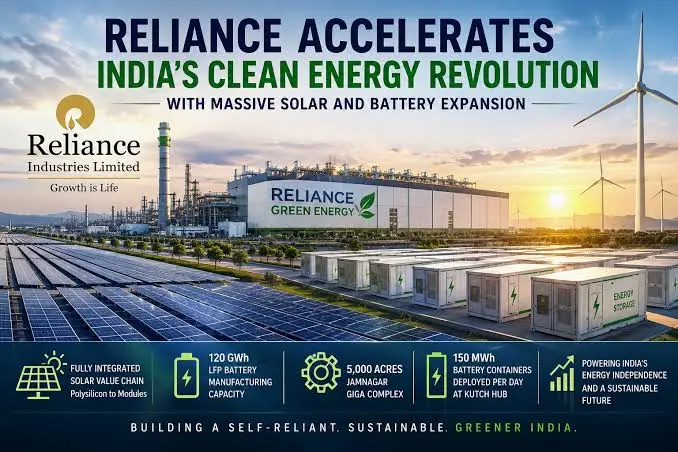

Japan to Back Reliance Industries' India Clean Ene...

02 Jul 2026, 12:26 AM

Meta Shares Surge 10% on Rumored AI Cloud Computin...

02 Jul 2026, 12:15 AM

FirstCry to Sell ₹3,000 Million Stake in Swara Bab...

02 Jul 2026, 12:05 AM

Embassy Developments to Consider Fund Raising via...

01 Jul 2026, 11:59 PM

Zee Entertainment Denies Rumors of ₹418 Crore FDI...

01 Jul 2026, 11:56 PMADVERTISEMENT

Top Stories

Japan to Back Reliance Industries' India Clean Ene...

02 Jul 2026, 12:26 AM

Meta Shares Surge 10% on Rumored AI Cloud Computin...

02 Jul 2026, 12:15 AM

FirstCry to Sell ₹3,000 Million Stake in Swara Bab...

02 Jul 2026, 12:05 AM