Loading market data...

ADVERTISEMENT

Latest Top News

Swiggy Shares Surge 4.3% On Strong Growth Signals And Strategic Expansion

Swiggy, India’s leading food delivery and quick commerce platform, saw its shares rise sharply by 4.3% amid growing investor optimism around the company’s expansion and solid revenue growth. This uptick comes on the back of encouraging quarterly performance and strategic moves that hi...

Stay Ahead – Explore Now! Fitch Rates IIFL Finance's USD500 Million Notes Final 'B+'

ADVERTISEMENT

Latest Updates

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

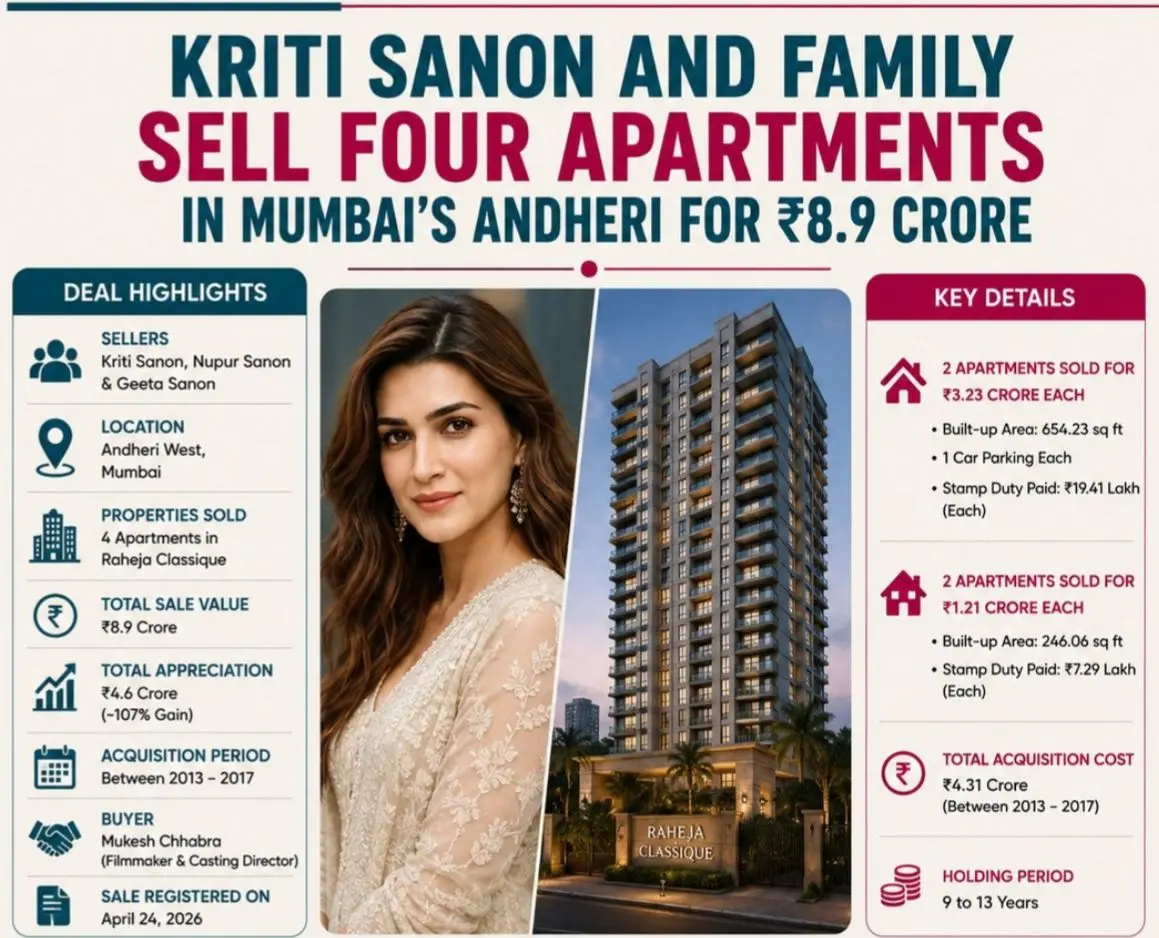

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PMADVERTISEMENT

Top Stories

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM