Loading market data...

ADVERTISEMENT

Latest Top News

Dalal Street Dials Down: Nifty 50 Sheds 0.35% in Risk-Off Mood

India’s benchmark equity index, the Nifty 50 (.NSEI), ended Tuesday’s trading session in the red, falling 0.35% as investors booked profits following recent gains and global cues remained mixed. The index closed at 24,363, down nearly 85 points from the previous session, reflecting a...

Stay Ahead – Explore Now! Star Power: Mercedes-Benz S-Class Facelift Set for India Launch

ADVERTISEMENT

Latest Updates

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

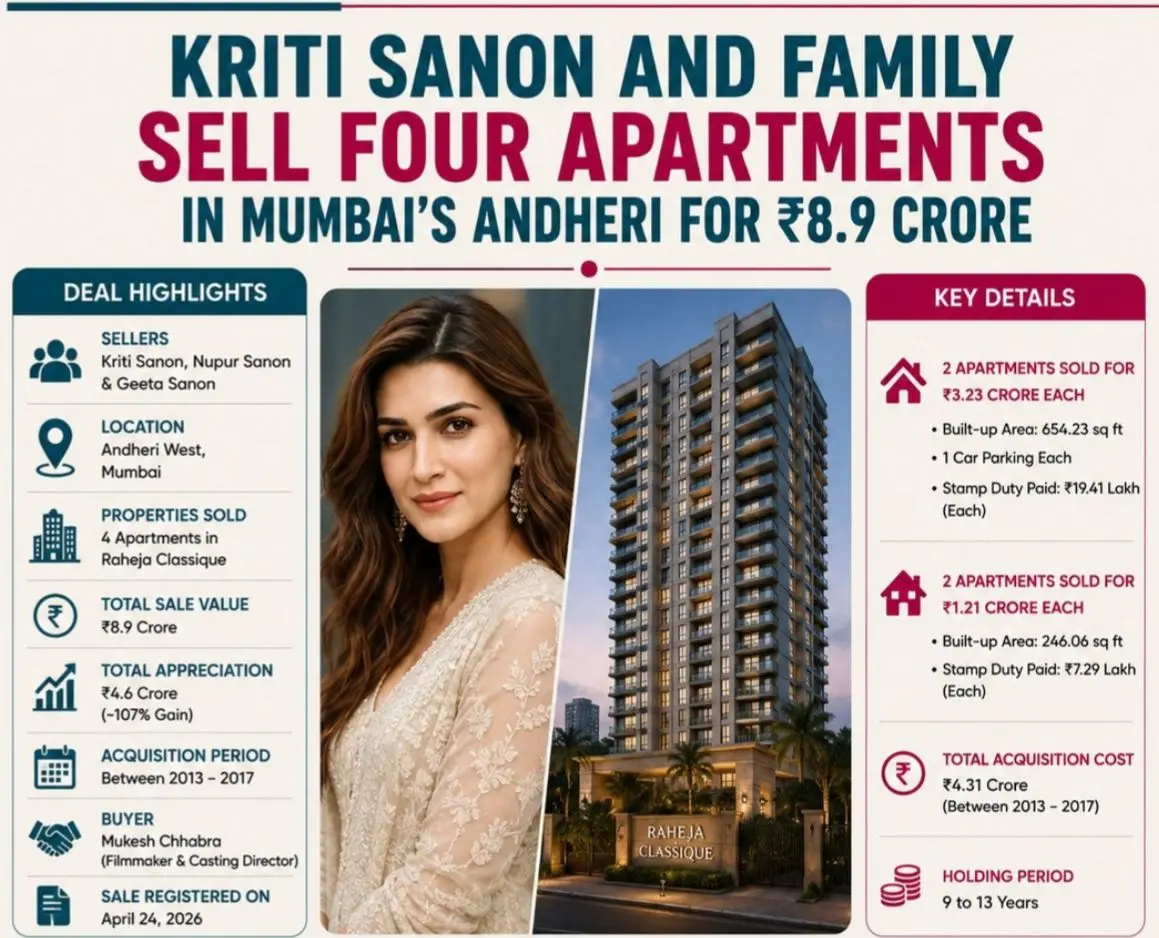

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM

AI Over the Hill: Gemini Picks Winner in Summer Tr...

15 Jun 2026, 11:36 PMADVERTISEMENT

Top Stories

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM