Loading market data...

ADVERTISEMENT

Latest Top News

Dhampur Bio Organics Slips into Red Despite Revenue Uptick in Q1 FY26

Mixed Start to the Fiscal Year Amid Margin Compression

Dhampur Bio Organics Ltd reported its consolidated financial results for the quarter ended June 2025, revealing a challenging start to FY26. While revenue from operations rose to Rs 784 crore, the company posted a net loss of Rs 22 crore,...

Stay Ahead – Explore Now! Styrenix Performance Materials Tax Demand of 43.8 Million Rupees Deleted

ADVERTISEMENT

Latest Updates

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

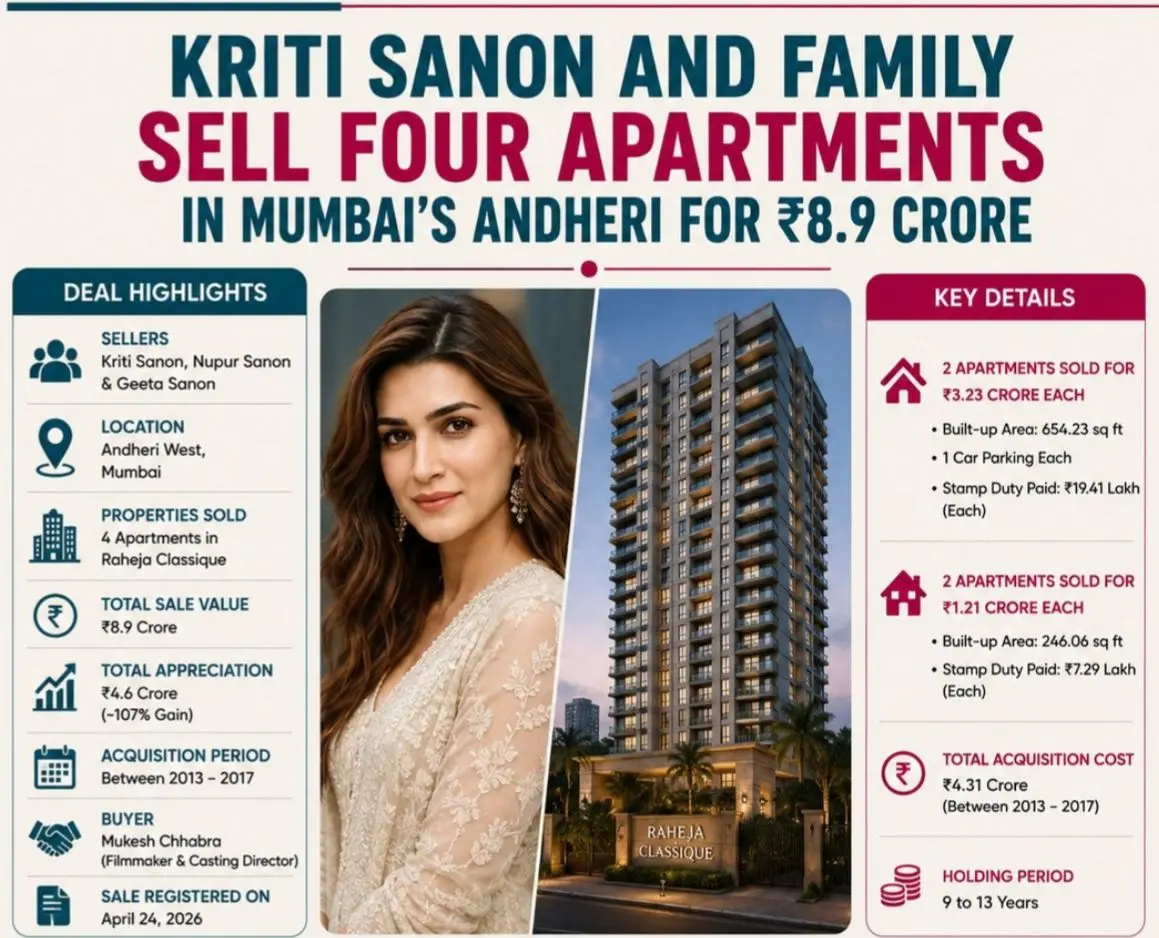

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM

AI Over the Hill: Gemini Picks Winner in Summer Tr...

15 Jun 2026, 11:36 PMADVERTISEMENT

Top Stories

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM