Loading market data...

ADVERTISEMENT

Latest Top News

Emkay Global Highlights Paytm’s Ring-Fenced Structure Protecting Core Business From PPBL Fallout

Emkay Global has reassured investors that Paytm’s core business remains unaffected despite the Reserve Bank of India (RBI) cancelling the licence of Paytm Payments Bank Ltd (PPBL) effective April 24, 2026. The brokerage emphasized that Paytm’s operations, including UPI, QR payments, Soundbox, and merchant services, will continue seamlessly.

Stay Ahead – Explore Now! Major Stocks Turn Ex-Dividend This Week: HDFC Bank, Tata Tech in Focus

ADVERTISEMENT

Latest Updates

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

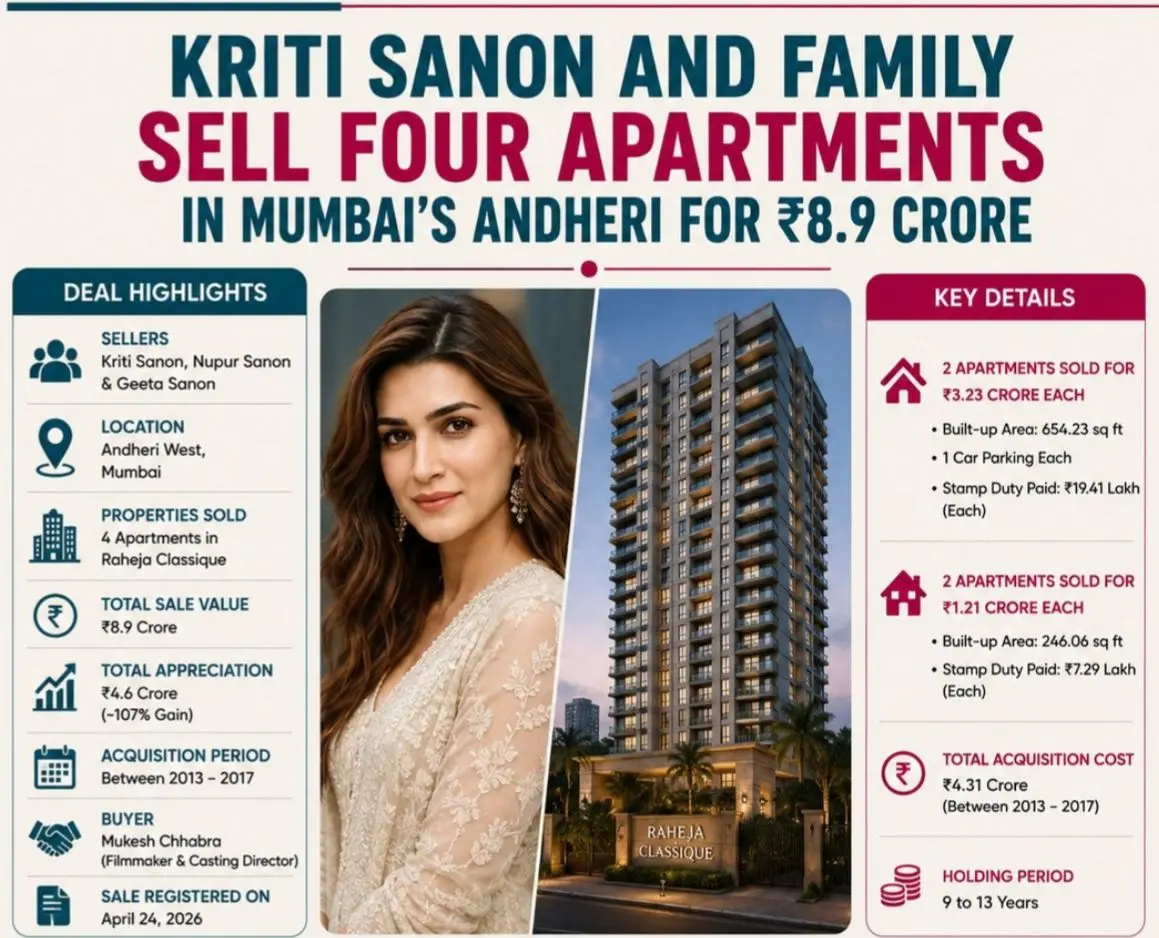

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM

AI Over the Hill: Gemini Picks Winner in Summer Tr...

15 Jun 2026, 11:36 PM

Track to Uttarakhand: Namo Bharat Expansion Nears...

15 Jun 2026, 10:18 PMADVERTISEMENT

Top Stories

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM