Loading market data...

ADVERTISEMENT

Latest Top News

Fitch Sounds the Alarm – The Billion-Dollar Split Shaping Asia’s Thermal Power Future

Asia-Pacific’s (APAC) thermal power generation companies (gencos) are about to see sharply diverging leverage trends, Fitch Ratings announced on August 13, 2025. As the sector pours billions into capital expenditure, the pace and type of investments are reshaping credit profiles—and t...

Stay Ahead – Explore Now! 'Raakh' Review: Ali Fazal-Sonali Bendre's Show Kills You With the Horrors of Life

ADVERTISEMENT

Latest Updates

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

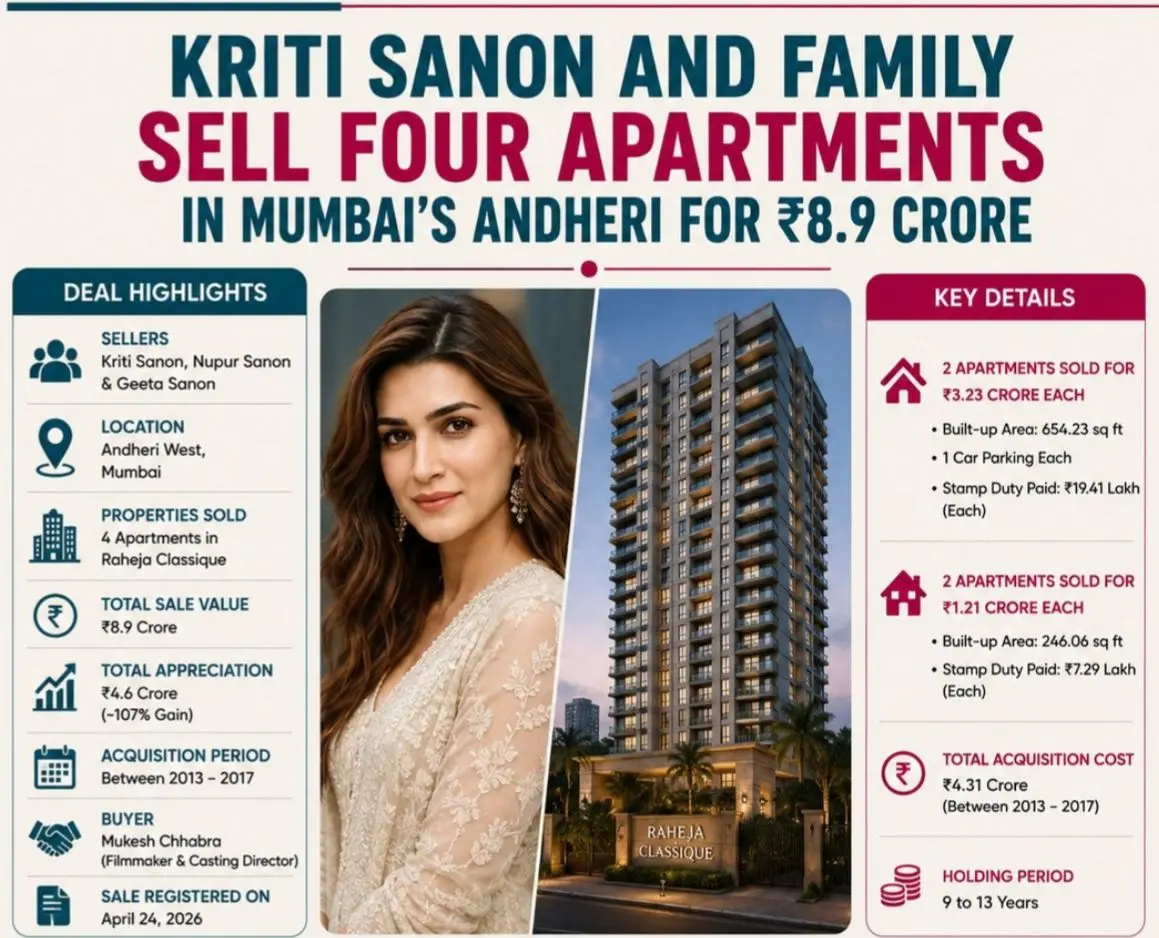

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM

AI Over the Hill: Gemini Picks Winner in Summer Tr...

15 Jun 2026, 11:36 PMADVERTISEMENT

Top Stories

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM