Loading market data...

ADVERTISEMENT

Latest Top News

Home Loan Happiness: RBI’s Rate Cut Delivers a Welcome Windfall

Indian home loan borrowers are smiling as the Reserve Bank of India (RBI) cut the repo rate by 50 basis points (bps) to 5.5% in its recent monetary policy, a total of 100 bps (1%) cut since February 2025. Combined with a 100 bps cut in the Cash Reserve Ratio (CRR), this action is going to bring h...

Stay Ahead – Explore Now! PCBL Chemical Ltd Commissions New Specialty Production Line at Mundra

ADVERTISEMENT

Latest Updates

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

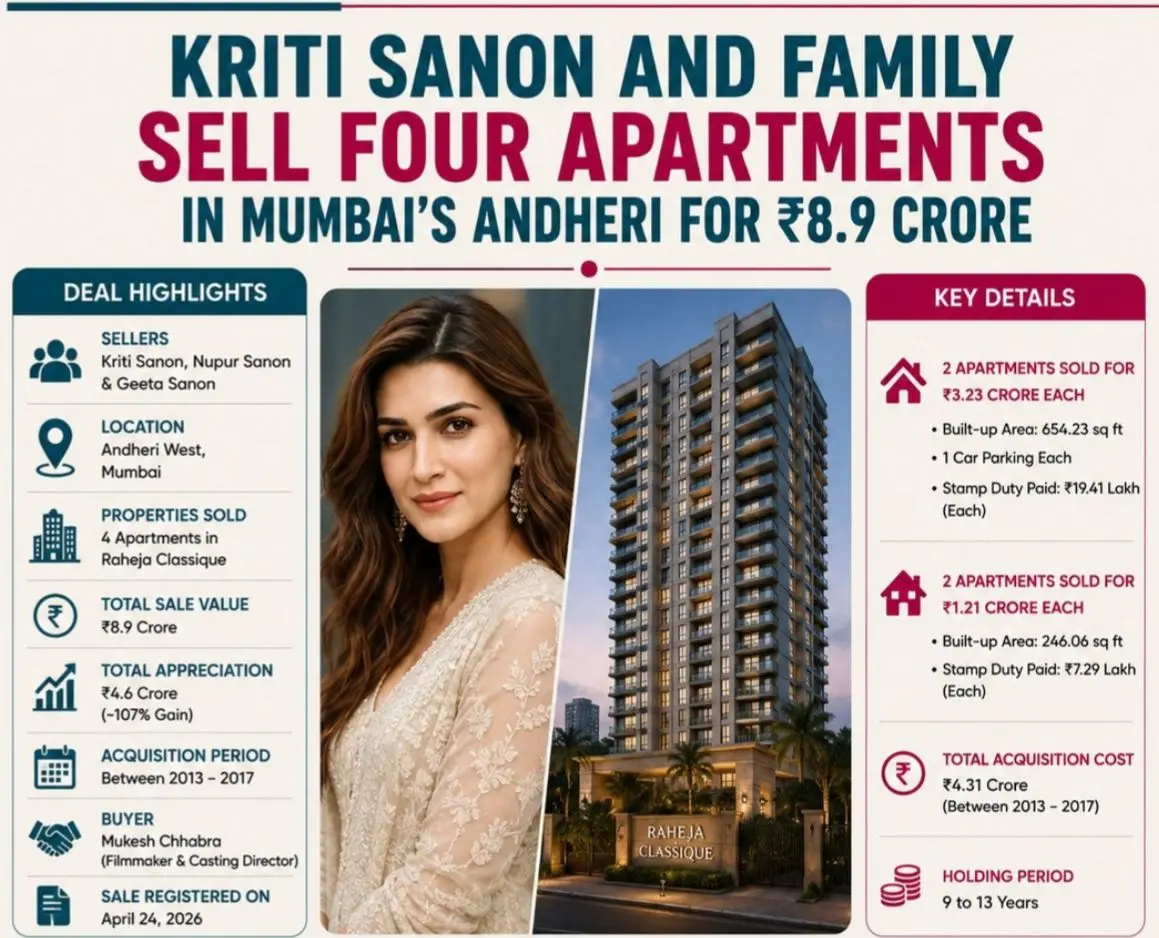

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM

AI Over the Hill: Gemini Picks Winner in Summer Tr...

15 Jun 2026, 11:36 PM

Track to Uttarakhand: Namo Bharat Expansion Nears...

15 Jun 2026, 10:18 PMADVERTISEMENT

Top Stories

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM