Loading market data...

ADVERTISEMENT

Latest Top News

Modern Insulators Sparks Stability in Q1 with ₹152.2 Million Profit on ₹1.41 Billion Revenue

Modern Insulators Ltd has reported a steady financial performance for the June quarter of FY26, reinforcing its position in the industrial ceramics and electrical insulation space. The company posted a consolidated revenue from operations of ₹1.41 billion and a net profit of ₹152.2 million, refle...

Stay Ahead – Explore Now! Global Chess League Season 4 to Be Hosted in Bengaluru

ADVERTISEMENT

Latest Updates

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

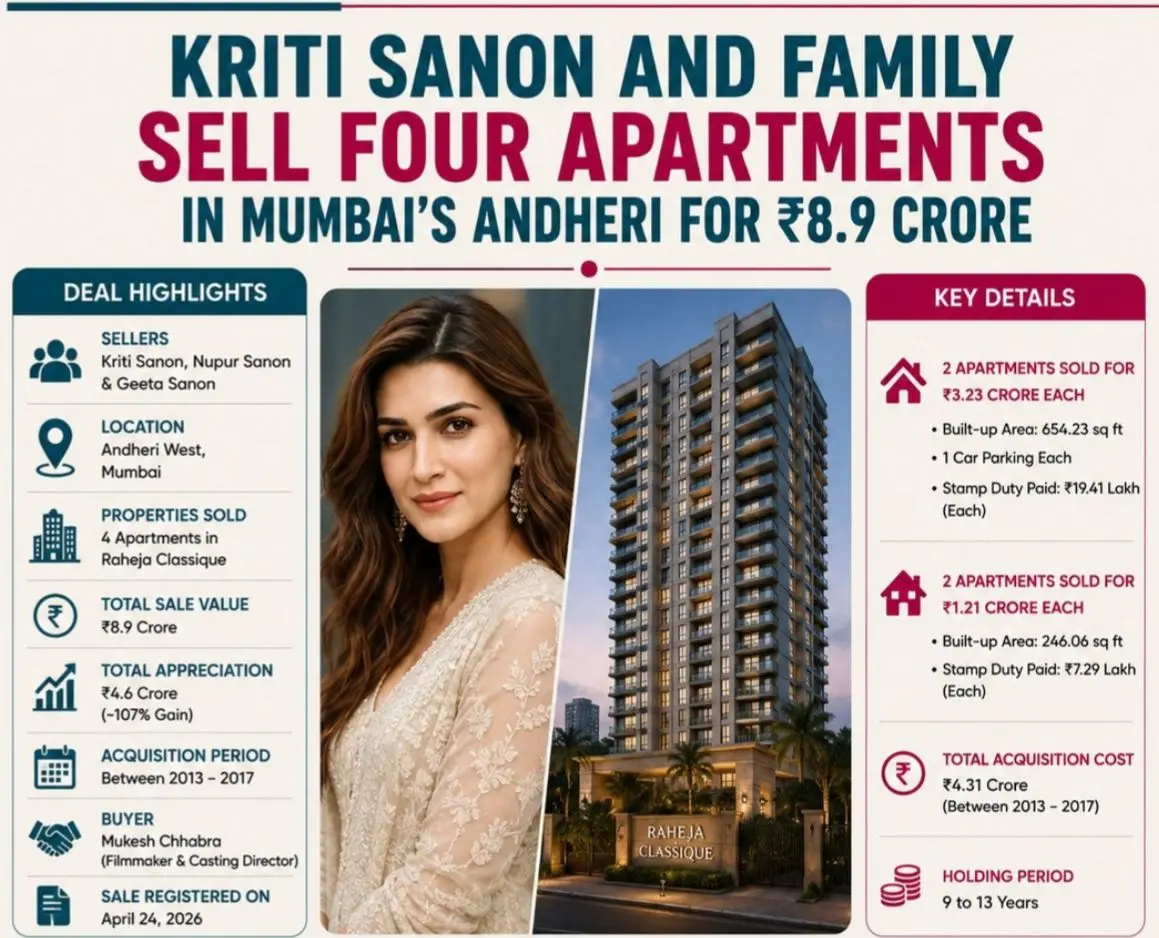

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PMADVERTISEMENT

Top Stories

Leapfrog Engineering Services IPO Bound: Price Ban...

15 Jun 2026, 11:50 PM

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM