The global financial technology sector is undergoing an infrastructure overhaul to adapt to tighter venture capital markets. Driven by the need for structural margin protection, the next fintech stack will be built on AI, cloud, APIs and cost discipline, helping companies eliminate middle-office waste and build highly profitable modular banking systems.

SAN FRANCISCO — Global financial institutions and venture capital firms are aggressively overhauling their underlying software architectures to survive a prolonged downturn in private tech valuations. According to a joint sector report published by the Federal Reserve Board and McKinsey & Company on Thursday, June 18, 2026, the financial technology industry has reached an operational inflection point. Following a 40% contraction in early-stage funding over the past two fiscal years, enterprise software architects are systematically abandoning legacy codebases. Industry data confirms that the next fintech stack will be built on AI, cloud, APIs and cost discipline as companies pivot from growth-at-all-costs strategies toward strict unit-economic profitability.

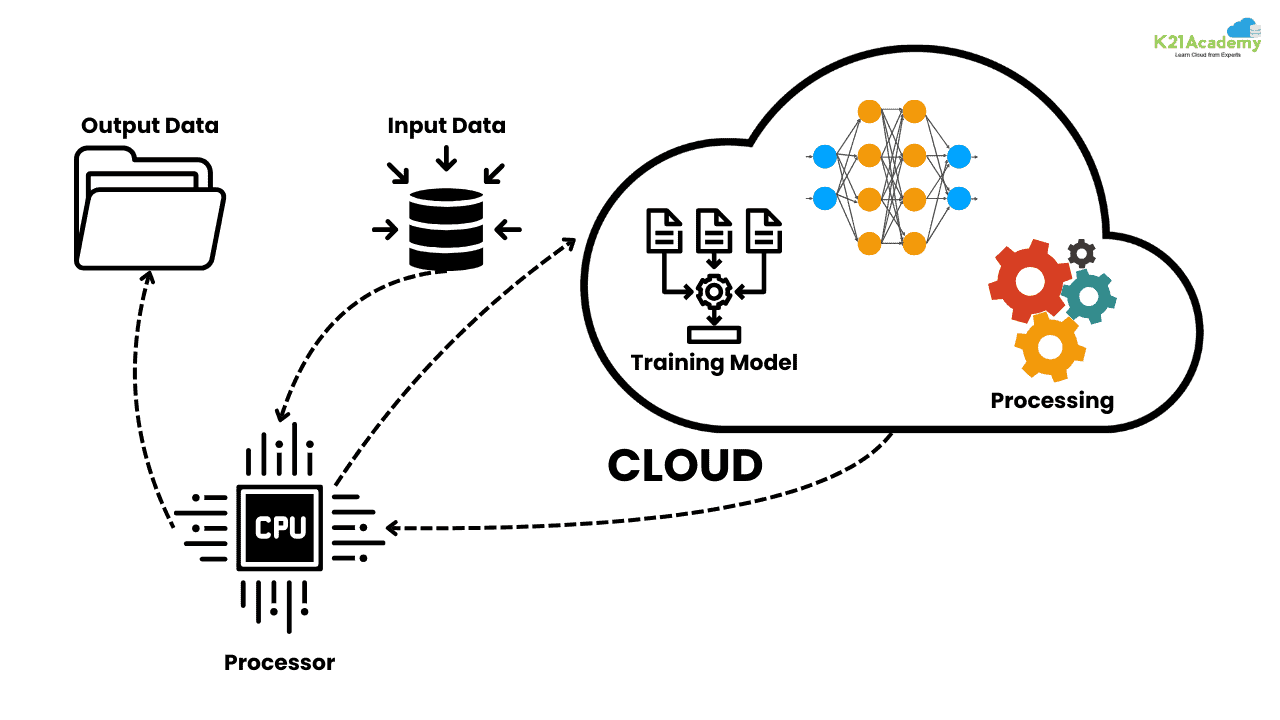

Artificial Intelligence Replaces Rigid Middle-Office Infrastructure

The integration of generative artificial intelligence and specialized machine learning models is fundamentally restructuring the core application layer of the next fintech stack. Historically, financial technology startups relied on large, human-intensive operations teams to manage compliance, know-your-customer (KYC) verifications, and credit underwriting.

Data from the Federal Financial Institutions Examination Council (FFIEC) reveals that modern platforms utilizing AI-driven middleware have successfully reduced their structural compliance overhead by 65%. Rather than relying on static, rule-based software, the next fintech stack implements real-time natural language processing and deep learning engines to monitor transactions for illicit cross-border flows. This shift enables institutions to scale their transaction volumes exponentially without an equal, linear expansion in administrative headcount.

Cloud Native Architectures Overthrow On-Premises Core Banking

The structural transition to fully elastic, cloud-native frameworks has evolved from a progressive choice into a mandatory fiscal requirement. Traditional financial services frequently burned through substantial capital reserves maintaining hybrid data centers or rigid multi-year on-premises server contracts.

According to regional regulatory filings submitted to the Securities and Exchange Commission (SEC), major payment processors are systematically transitioning their ledger engines to hyper-scalable public cloud environments. By leveraging dynamic server allocation models, firms can scale their processing capabilities up during peak trading intervals—such as major global sports tournaments or retail shopping holidays—and immediately scale them back down during low-traffic overnight hours. This structural elasticity directly prevents over-provisioning, allowing technology firms to align their real-time compute expenditures with volatile transaction revenues.

Advanced APIs Drive Modular Open-Banking Systems

The third foundational pillar of the modern operational framework centers on microservices linked by advanced Application Programming Interfaces (APIs). In previous software iterations, developers built massive, interconnected platforms where a single database malfunction could freeze an entire consumer ecosystem.

By utilizing modular, specialized APIs, modern digital banks can entirely offload their peripheral financial services to specialized third-party providers. A digital banking application no longer needs to construct its own cross-border remittance, stock brokerage, or cryptocurrency custody engines from scratch. Instead, it securely plugs directly into external API networks. The modular approach insulates the underlying banking core from unnecessary system vulnerabilities while dramatically shortening the time-to-market for consumer-facing features.

The Strategic Enforcement of Rigorous Cost Discipline

The defining element binding these technological changes together is an industry-wide enforcement of rigorous cost discipline. During the peak venture capital cycle of the early 2020s, fintech enterprises prioritized user acquisition velocity over actual net margins, frequently absorbing substantial transaction processing losses to expand their superficial market share.

The current macroeconomic environment of elevated central bank interest rates has entirely closed that avenue of growth. Analysis from the Bank for International Settlements (BIS) confirms that institutional investors are heavily penalizing firms with negative operating cash flows. Consequently, the engineering design of the next fintech stack treats structural cost efficiency as an essential architectural feature rather than a secondary consideration. Every lines of code, database query, and third-party vendor call is continuously audited for margin efficiency to ensure that gross margins remain reliably above 75%.

Official Sources Section

The engineering methodologies, investment parameters, software metrics, and institutional restructuring patterns cited in this report were compiled from joint research reports published by McKinsey & Company, public technology transition filings available via the U.S. Securities and Exchange Commission (SEC), and central bank digital infrastructure whitepapers issued by the Bank for International Settlements (BIS).

Quote Section

"According to officials managing global enterprise risk portfolios, the era of experimental software inflation in finance has concluded," the joint regulatory briefing notes. "The next fintech stack will be built on AI, cloud, APIs and cost discipline to ensure that digital financial platforms can withstand severe market cycles while maintaining clear pathways to profitability."

Why It Matters

The shift toward an optimized, highly disciplined financial software ecosystem has profound practical implications for everyday consumers, businesses, and international investors. When fintech companies eliminate structural infrastructure waste, they can afford to lower transfer fees, provide more competitive interest rates on digital deposit accounts, and extend credit lines to historically underserved small businesses. For institutional investors, a technology sector anchored by modular APIs, elastic cloud computing, and automated AI compliance provides a highly predictable, lower-risk asset class that delivers stable returns even during broader economic downturns.

Key Facts at a Glance

Architectural Pivot: Industry data indicates the next fintech stack will be built on AI, cloud, APIs and cost discipline to survive tighter capital markets.

Cost Reduction: Automated AI middleware has lowered compliance and manual middle-office processing costs by up to 65%.

Modular Infrastructure: Modern platforms use advanced APIs to lease niche financial microservices rather than spending millions building internal codebases.

Elastic Computing: Cloud-native ledger infrastructure allows tech firms to pay for processing power dynamically on a per-second basis, eliminating server waste.

FAQ Section

Q: What exactly does "the next fintech stack" refer to? A: A fintech stack is the underlying combination of software, operating systems, databases, APIs, and cloud servers that power digital banking, payment processing, and online investment applications. The "next" stack represents the modern architecture required to achieve profitability in today's high-interest-rate environment.

Q: How does building on APIs save money for a financial tech firm? A: Instead of hiring internal software engineering teams to build complex tools like international currency conversion or security verification from scratch, companies use third-party APIs to instantly plug those functions into their existing apps, saving millions in development costs.

Q: Will this focus on cost discipline lead to a reduction in features for regular app users? A: No. In fact, by utilizing modular cloud systems and AI automation, digital financial platforms can introduce new consumer features much faster and at a lower operational cost, often leading to reduced transactional fees for end users.

Source: * Bank for International Settlements (BIS) Financial Innovation Archive