Loading market data...

ADVERTISEMENT

Latest Top News

Rare Earths Not So Rare Anymore: How India Averted a Crippling Crunch and Reclaimed Control

India recently averted what could have been a crippling shortage of rare earth minerals—vital components for electric vehicles (EVs), wind turbines, consumer electronics, and advanced military systems. This “near-disaster” was narrowly avoided through a combination of strategic...

Stay Ahead – Explore Now! Teen Innovator Pranjali Awasthi Builds Rs 100 Crore AI Venture

ADVERTISEMENT

Latest Updates

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

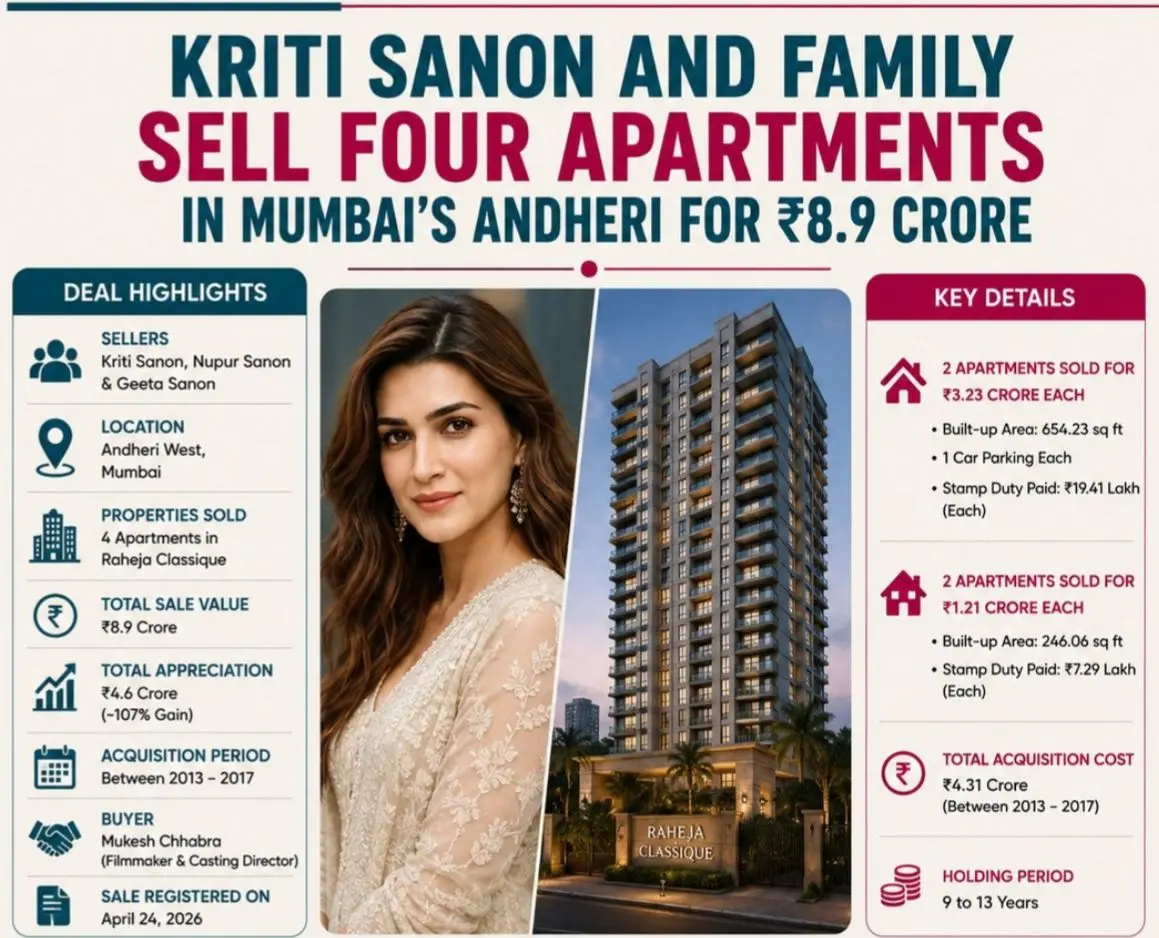

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PMADVERTISEMENT

Top Stories

Instamart Inks Growth: Dhanya Hemanth Raj Named Ma...

15 Jun 2026, 11:52 PM

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM