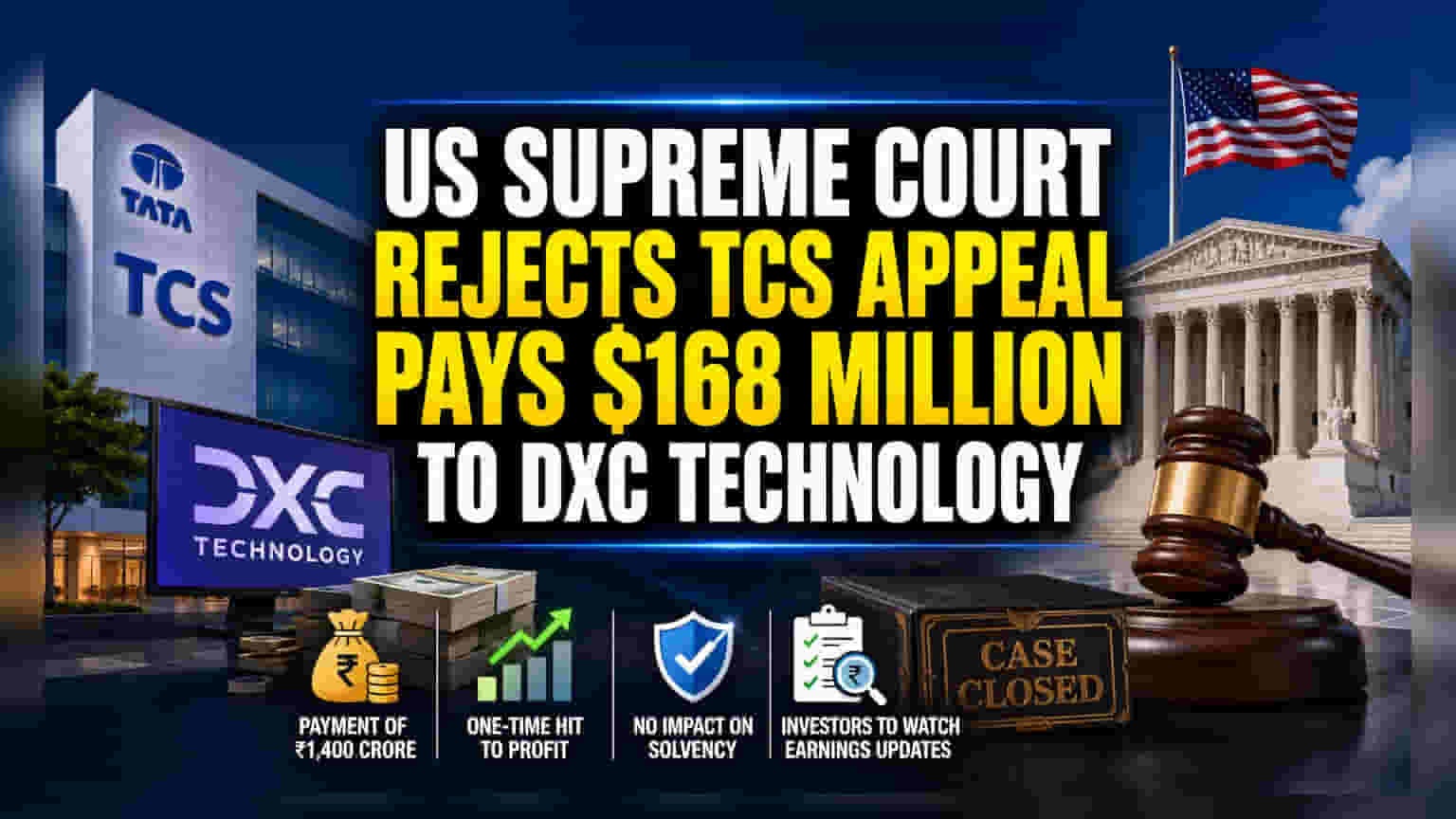

Tata Consultancy Services will book a $70 million one-time exceptional expense in Q1 FY2027 following the US Supreme Court's June 15, 2026 decision rejecting its appeal. The ruling finalizes a $168 million intellectual property lawsuit brought by DXC Technology, forcing India's largest IT exporter to provision remaining legal liabilities.

MUMBAI — In a definitive legal setback in the United States, India's largest information technology services exporter, Tata Consultancy Services Limited (TCS), has confirmed it will book a one-time exceptional expense of $70 million (approximately ₹585 crore) in its financial results for the first quarter of fiscal year 2027. The financial provision follows a decision on Monday, June 15, 2026, by the U.S. Supreme Court, which denied a petition filed by TCS to review and overturn a $168 million damages award won against it by Virginia-based rival DXC Technology Company. The final ruling exhausts the company's judicial options in North America, bringing a close to an intense multi-year legal battle surrounding intellectual property misappropriation.

Evolution of the DXC Intellectual Property Litigation

The core of the legal dispute traces back to a 2019 civil lawsuit initiated in a Dallas federal court by DXC Technology's predecessor entity, Computer Sciences Corporation (CSC). The plaintiff alleged that TCS had hired roughly 2,200 employees originally stationed at financial services firm Transamerica. The complaint stated that TCS subsequently utilized those individuals' technical access permissions and specialized expertise regarding CSC’s proprietary life-insurance software to build a competing software platform.

While TCS strongly contested the allegations throughout the proceedings arguing that the underlying system specifications were not legally classified as secrets and that its personnel had accessed the software infrastructure through legitimate commercial paths a federal jury issued an advisory verdict in 2023 finding the firm had willfully and maliciously misappropriated trade secrets.

The original financial penalty was formally set by U.S. District Judge Brantley Starr in 2024 at $168 million, which comprised:

Compensatory Damages: Calculated at $56 million, anchored on concepts of unjust enrichment.

Punitive Damages: Assessed at $112 million following judicial determinations of malicious intent.

The ruling was subsequently upheld by the New Orleans-based 5th U.S. Circuit Court of Appeals in late 2025, leading to the final unsuccessful appeal before the nation's high court.

Technical Allocation and Financial Impact Architecture

In an official regulatory disclosure submitted under Regulation 30 of the SEBI Listing Obligations to both the National Stock Exchange of India (NSE) and BSE Limited, TCS Corporate Secretary Yashaswin Sheth clarified the structural accounting changes resulting from the final dismissal.

The technology exporter had previously recognized a balance sheet provision amounting to $150 million across earlier audited timelines to mitigate the impending liability. Following the denial of the writ of certiorari by the U.S. Supreme Court, the enterprise will now recognize an additional provision of $70 million during the April-to-June quarter of FY2027 to satisfy the residual damages balance, accumulating interests, and related overseas legal administration costs.

EBIT Margin Impact: Institutional research desks calculate that the $70 million incremental charge will be treated entirely as an exceptional item. This accounting movement is projected to create a short-term compression of approximately 10 to 15 basis points on the company's operating EBIT margins for Q1 FY2027.

Implications for Global IT Services Providers

The finality of this high-stakes verdict serves as an important precedent for Indian technology firms servicing the North American market, which remains the single largest destination for domestic export revenue. Intellectual property lawyers note that the U.S. Supreme Court's refusal to interfere reinforces strict regulatory frameworks governing "unjust enrichment" parameters, meaning plaintiffs can successfully claim structural damages even without providing itemized proof of real financial losses. For offshore delivery operations, the judgment underlines the critical importance of implementing strict, airtight compliance separation walls during large-scale workforce rebadging transitions.

Official Sources Section

The underlying details, chronological actions, and monetary metrics cited across this report are extracted directly from corporate disclosure file number TCS/SE/40/2026-27 submitted to Indian stock exchanges, public dockets published by the Supreme Court of the United States, and financial notifications verified by the Securities and Exchange Board of India (SEBI).

Quote Section

"According to officials representing the corporate secretarial division at TCS, the firm will execute the necessary provisions immediately to fully isolate its operational profit centers from the legal conclusion of the DXC litigation cycle."

Why It Matters

While the one-time financial charge poses a temporary drag on the immediate quarterly profit performance, it effectively eliminates a major, unresolved legal liability that has cast a shadow over the company’s enterprise software divisions for over six years. Clearing this long-standing issue allows management to stabilize its long-term financial guidance.

Key Facts at a Glance

Final Judgment: The U.S. Supreme Court denied the petition to review the $168 million total lower-court award.

Exceptional Item: TCS will book a fresh $70 million expense in Q1 FY2027 to cover the remaining damages, interest, and legal overheads.

Prior Provisions: The company had already set aside $150 million in its books for this specific case.

Core Accusation: The litigation stems from allegations that the company improperly used trade secrets from life-insurance software owned by DXC’s predecessor.

FAQ Section

1. Why did the U.S. Supreme Court reject the appeal from TCS?

The high court declined the petition for a writ of certiorari without comment, upholding the decisions of the lower appellate courts that found the company's actions constituted unjust enrichment regarding proprietary software.

2. Will this development impact the long-term dividend distribution of the company?

Market analysts indicate that since TCS maintains vast free cash flows and had already provisioned $150 million of the liability, this incremental $70 million charge is unlikely to damage core shareholder capital return structures.

3. What exactly is a "one-time exceptional expense"?

An exceptional expense is a material financial charge that arises from events outside the ordinary, day-to-day operations of a company. It is isolated on the profit and loss statement so investors can clearly separate regular business performance from non-recurring costs.

4. When will this legal loss be visible in the financial statements?

The financial impact will be officially recognized and published within the company's un-audited consolidated financial reports for the first quarter of the fiscal year 2027 (Q1 FY2027).

Source: