Loading market data...

ADVERTISEMENT

Latest Top News

Money Matters: Decoding the Right Time to Worry About Your Finances

In today's financial world, understanding when to worry about money can make a significant difference in maintaining stability and achieving peace of mind. It's not just about reacting to problems but proactively addressing key concerns that could lead to financial difficulties.

...

Stay Ahead – Explore Now! Seven Lush Monsoon Treks Near Hyderabad Within 250 KM to Explore

ADVERTISEMENT

Latest Updates

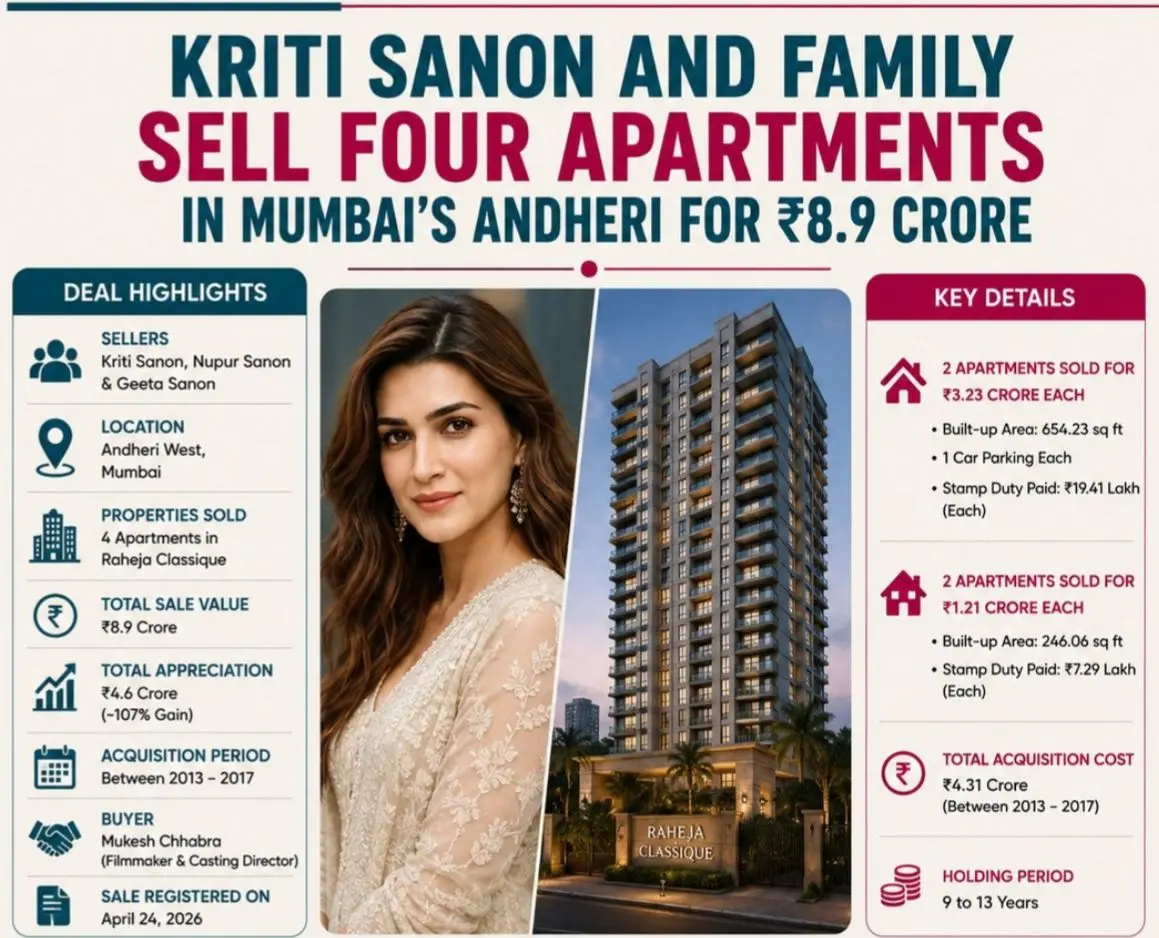

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM

AI Over the Hill: Gemini Picks Winner in Summer Tr...

15 Jun 2026, 11:36 PM

Track to Uttarakhand: Namo Bharat Expansion Nears...

15 Jun 2026, 10:18 PM

From Silt to Sustainability: BMC Starts Rejuvenati...

15 Jun 2026, 02:01 PMADVERTISEMENT

Top Stories

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM

AI Over the Hill: Gemini Picks Winner in Summer Tr...

15 Jun 2026, 11:36 PM