Loading market data...

ADVERTISEMENT

Latest Top News

PPF Vs EPF Vs NPS: Comparing India’s Top Retirement Schemes

PPF, EPF, and NPS are India’s three most popular retirement savings schemes, each offering unique benefits. EPF is salary-linked and compulsory for salaried employees, PPF is a government-backed long-term savings option, and NPS combines equity and debt exposure with flexible tax advantages. Choosing the right one depends on income type, risk appetite, and retirement goals.

Stay Ahead – Explore Now! Jaiprakash Associates Set to Delist from BSE and NSE

ADVERTISEMENT

Latest Updates

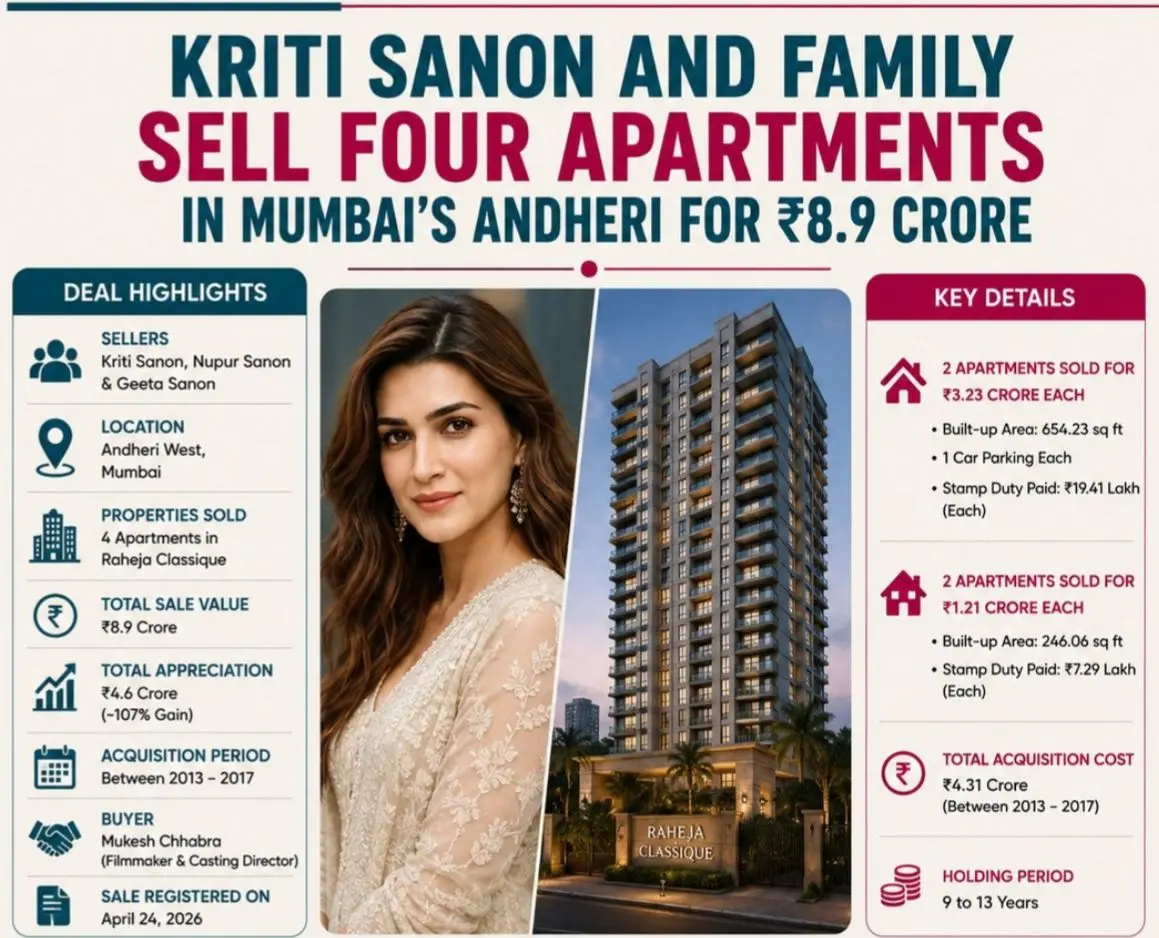

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM

AI Over the Hill: Gemini Picks Winner in Summer Tr...

15 Jun 2026, 11:36 PM

Track to Uttarakhand: Namo Bharat Expansion Nears...

15 Jun 2026, 10:18 PM

From Silt to Sustainability: BMC Starts Rejuvenati...

15 Jun 2026, 02:01 PMADVERTISEMENT

Top Stories

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM

AI Over the Hill: Gemini Picks Winner in Summer Tr...

15 Jun 2026, 11:36 PM