Loading market data...

ADVERTISEMENT

Latest Top News

What’s Shielding Indian Companies From U.S. Tariffs? Fitch Has the Answers

Fitch Ratings has projected a positive outlook for Indian corporates in FY26, citing improved credit metrics driven by stronger EBITDA margins and resilient financial buffers. Despite global trade tensions and higher U.S. tariffs, the agency expects only limited direct impact on India Inc., thank...

Stay Ahead – Explore Now! Tracking Trackers: Indian Railways Welcomes 43,781 New Recruits

ADVERTISEMENT

Latest Updates

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

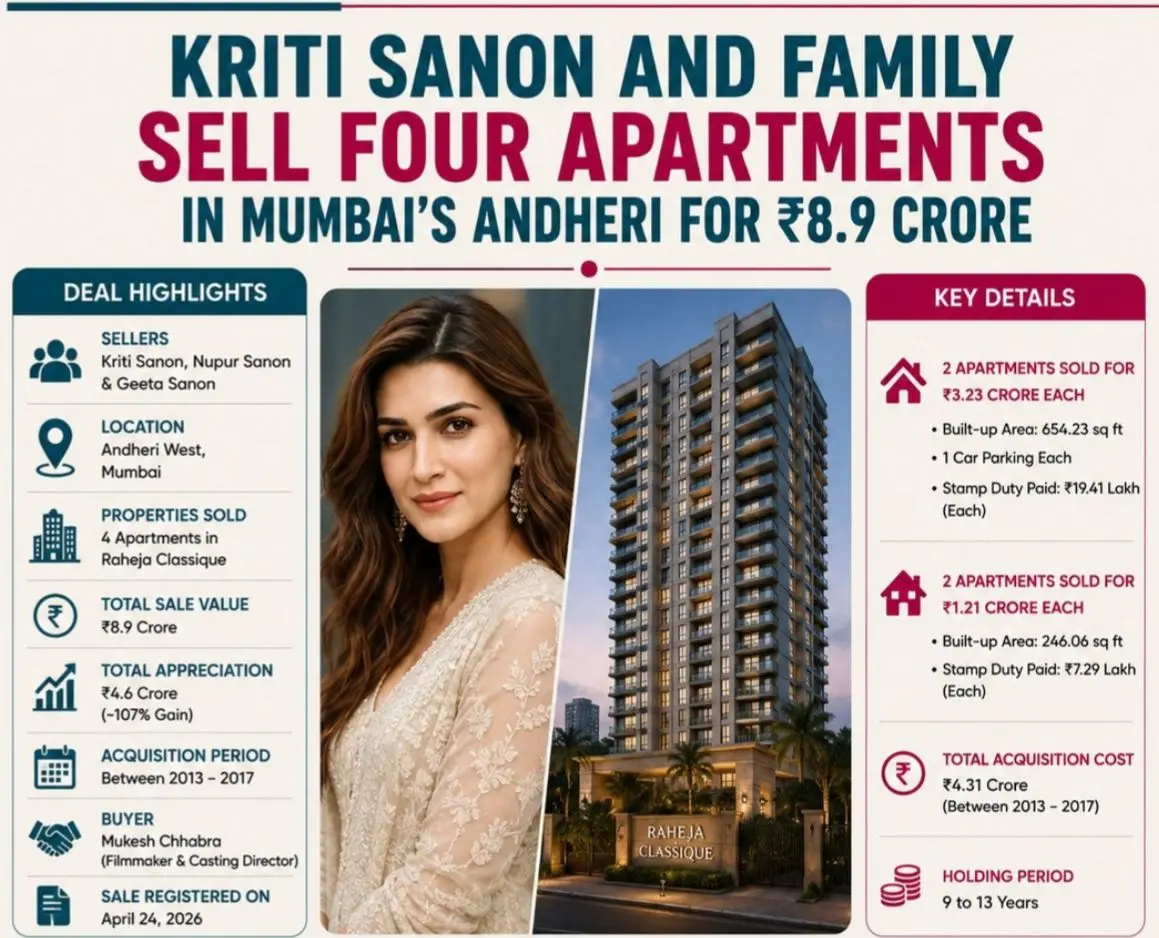

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM

Banking on Trust: RBI Bans Coercive Bundling and A...

15 Jun 2026, 11:39 PM

AI Over the Hill: Gemini Picks Winner in Summer Tr...

15 Jun 2026, 11:36 PMADVERTISEMENT

Top Stories

Sri Lanka 'A' Edge India 'A' in Heated Super Over...

15 Jun 2026, 11:47 PM

Mercedes-Benz India Steers Past Headwinds to Fuel...

15 Jun 2026, 11:45 PM

Sanon’s Andheri Asset Action: Family Bags ₹4.6 Cr...

15 Jun 2026, 11:42 PM