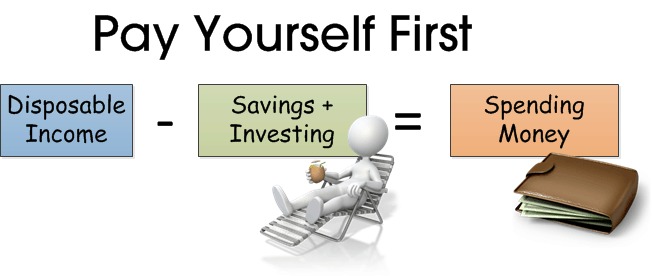

The “Pay Yourself First” budgeting method prioritizes savings by allocating a portion of income before expenses. Often structured as the 80/20 rule, it ensures consistent wealth-building and financial discipline. Automation enhances success, while flexibility allows customization. Despite challenges, it remains a powerful tool for long-term financial stability.

In today’s fast-paced financial environment, managing money effectively is more crucial than ever. One method gaining traction among financial planners and everyday savers alike is the “Pay Yourself First” budgeting approach. Unlike traditional budgeting, which often prioritizes expenses before savings, this method flips the script: it ensures that savings and investments are secured before discretionary spending begins.

Key Highlights

Core Principle: The “Pay Yourself First” method requires individuals to set aside a fixed percentage of income for savings immediately upon receiving their paycheck. This ensures that savings are treated as a non-negotiable expense rather than an afterthought.

80/20 Rule: A common framework is the 80/20 budget, where 20% of income is directed toward savings and debt repayment, while the remaining 80% covers living expenses and discretionary spending.

Reverse Budgeting Concept: This approach is often referred to as reverse budgeting, because instead of planning expenses first, individuals prioritize long-term financial goals such as emergency funds, retirement accounts, or investments.

Automation Advantage: Experts recommend automating transfers to savings accounts or investment vehicles. This reduces decision fatigue and ensures consistency, making it easier to stick to financial goals.

Flexibility: While 20% is a popular benchmark, individuals can adjust the percentage based on their financial situation, gradually increasing savings as income grows.

Why It Matters

The “Pay Yourself First” method is particularly effective because it removes the temptation to overspend. By treating savings like a mandatory bill, individuals build financial resilience and create a safety net for emergencies. Over time, this strategy helps in wealth accumulation, debt reduction, and retirement planning.

Financial advisors emphasize that this method is especially useful for young professionals starting their careers. By embedding savings habits early, individuals can leverage the power of compounding to grow wealth significantly over decades.

Risks and Challenges

While the method is straightforward, there are potential challenges:

Cash Flow Constraints: For individuals with tight budgets, allocating 20% upfront may feel restrictive. Experts suggest starting small—perhaps 5%—and gradually increasing the percentage.

Unexpected Expenses: Emergencies or irregular expenses can disrupt savings plans. Maintaining a separate emergency fund is critical to avoid dipping into long-term savings.

Discipline Required: The success of this method hinges on consistency. Without automation or strong financial discipline, individuals may revert to old spending habits.

Industry Context

The rise of fintech apps and digital banking has made the “Pay Yourself First” method easier to implement. Many platforms now offer automatic savings features, rounding up transactions or scheduling transfers to savings accounts. This technological support aligns perfectly with the philosophy of prioritizing savings before spending.

Investor and Consumer Outlook

Analysts believe that widespread adoption of this method could improve household financial health, reduce reliance on credit, and foster long-term investment culture. For consumers, it represents a practical, low-effort way to achieve financial stability without complex budgeting spreadsheets.

Sources: Bankrate, Thrivent, The Ways to Wealth